Cycling's Appeal to Private Equity

Why the cycling industry might be on the cusp of increased M&A activity and what it means for brands

Over the last two years, my newsfeed has been filled with stories about turbulence in the cycling industry. Whether it’s companies like Trek working through excess inventory from the COVID boom, Canyon being marked down by its holding company GBL, or mounting concerns over tariffs, the industry has felt unstable.

A common theme is that the largest brands appear to be struggling the most. In previous editions of Built on Bikes, I’ve highlighted how emerging brands with lean operating structures have often outperformed their bigger competitors in efficiency and adaptability. Companies like Pas Normal Studios and Ventum have focused on specific corners of the market and scaled in a more sustainable way over the last five years.

Now that the COVID surge is firmly behind us, larger brands are trying to restore healthy margins and regain profitability. Smaller brands, meanwhile, seem to be operating business as usual, staying lean and concentrating on brand development and steady growth.

One of the biggest differences between large and small brands during this period has been outside capital. Many smaller brands are bootstrapped or lightly funded, while several larger players were swept up in private equity activity during the COVID boom. Holding companies acquired brands in an effort to scale operations, meet surging demand, and extract value from already strong names. The upside, however, was short-lived.

High-profile deals such as GBL’s acquisition of Canyon and RZC Investments’ purchase of Rapha have faced criticism. Canyon leaned heavily into mass direct-to-consumer scale, and service quality appeared to decline post-acquisition. Rapha, as I’ve written about before, seemed to drift from some of the brand qualities that defined its rise in the 2010s. It’s no surprise that many cycling enthusiasts now view private equity involvement with skepticism.

The prevailing narrative has become simple: large acquisitions lead to profit-first thinking at the expense of quality and heritage. While I understand that sentiment, I think it misses an important nuance. Not all acquisitions are destructive. Some smaller, strategic deals have actually delivered meaningful benefits to consumers.

2026 and 2027 could be pivotal years for the cycling industry, particularly if we see a renewed wave of mergers and acquisitions. There will probably be monster deals similar to Canyon’s, but I think the real opportunity lies elsewhere, in smaller brands that have already proven sustainability and built strong, recognizable identities.

And before anyone jumps to conclusions, I’m not on the side of the investor. I think these types of deals could be incredibly beneficial to the brands we love and to us as consumers. Today I want to discuss how it could look and work.

What is the market telling us?

We know there was a COVID boom followed by a sharp decline, but now that things have stabilized, where is the industry heading? Will the entire market struggle alongside the biggest brands, or will a new wave of smaller brands emerge as the next industry leaders?

It is difficult to predict. But if recent history tells us anything, the cycling industry appears primed for another phase of private market activity.

In 2024, investment bank Houlihan Lokey and management consulting firm Kearney released a comprehensive report on M&A activity in the cycling industry, analyzing trends from 2020 through 2024. It is worth reading in full, but here are the key takeaways.

M&A ebb and flow

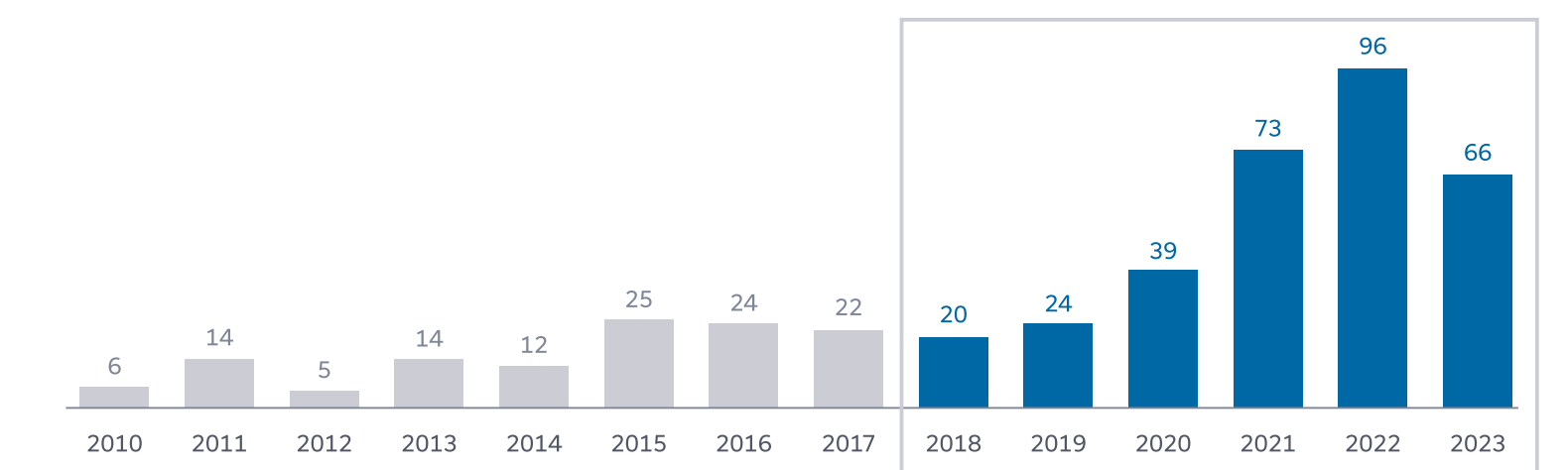

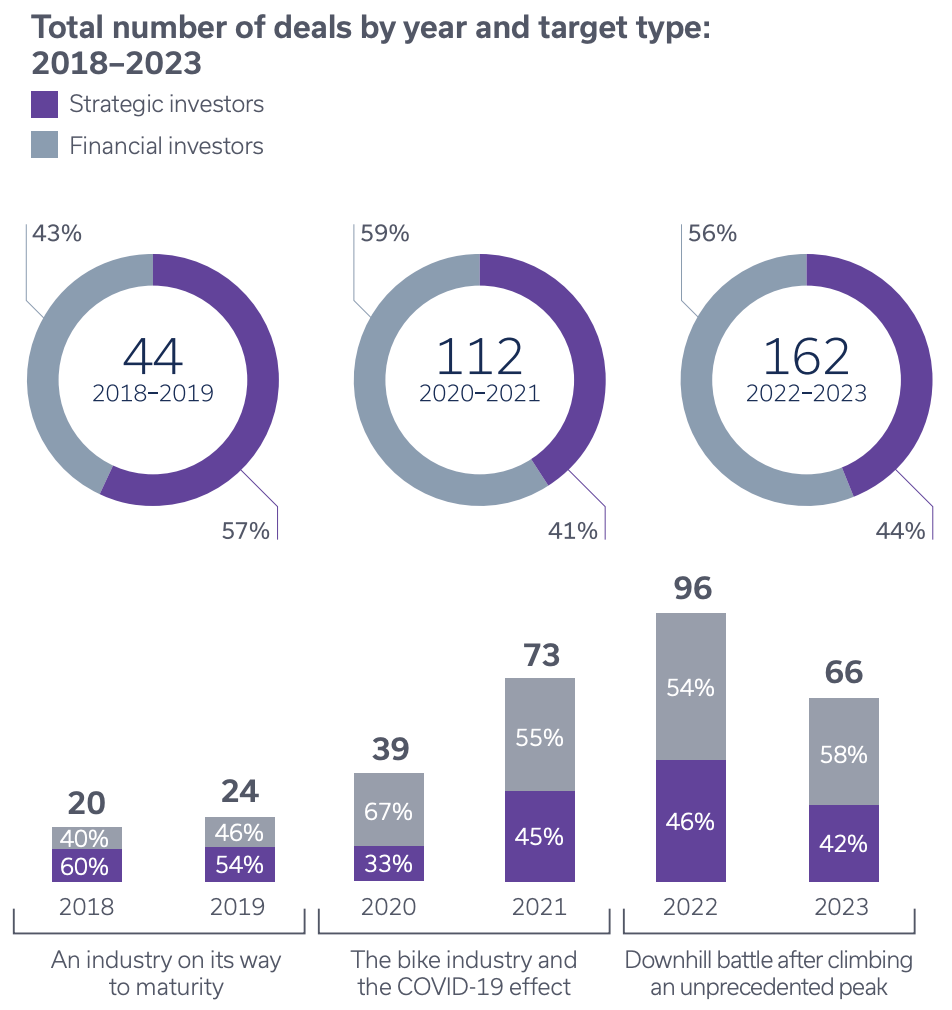

M&A activity peaked in 2022, riding the momentum of the COVID boom years in 2020 and 2021. There were 96 transactions in 2022. In 2023, that number dropped sharply to 66. For comparison, between 2015 and 2019, annual M&A activity typically ranged from 20 to 25 transactions.

That contrast underscores just how significant the COVID boom was. So does this mean we are heading back to historically low M&A volumes? Not necessarily.

As part of the report, more than 30 industry executives and 10 financial investment firms were interviewed. The prevailing sentiment was that activity is unlikely to drop back to pre-COVID levels. Houlihan Lokey forecasted a “gradual recovery with significant upside in the medium to long term” and noted that “2026 and 2027 mark pivotal years for increased M&A activity.”

The timing aligns with the typical lifecycle of a private equity investment. Firms generally aim to create value over a three to six year period before exiting. That framework lines up closely with investments made during the 2020 and 2021 boom. As those assets mature and the market stabilizes, exits will likely increase, and new investors may enter the space as well.

Strategic vs. financial investment

The type of M&A activity can be just as important as the volume of transactions, because structure often determines what happens to a brand after the deal closes. Broadly speaking, there are two categories worth focusing on: financial and strategic.

Financial investments typically involve private equity or other outside investment firms acquiring a company outright or taking a majority stake. In most cases, the company’s leadership team remains in place, while the board expands to include new stakeholders.

The expectation is straightforward. With additional capital and operational oversight, the company should grow faster, improve margins, and ultimately become more valuable ahead of a future exit.

Strategic investments usually take the form of mergers or acquisitions where one brand is absorbed into another operating company. The core idea is synergy. Shared R&D, combined distribution, and overlapping customer bases are meant to create efficiencies and unlock growth that would be difficult independently.

A recent example is Strava’s acquisition of Runna, where product integration and audience overlap were clear drivers of the deal.

Since 2020, the split between financial and strategic deals has remained relatively balanced:

2020: 67% financial vs 33% strategic

2021: 55% financial vs 45% strategic

2022: 54% financial vs 46% strategic

2023: 58% financial vs 42% strategic

While fairly even, financial investments have consistently edged out strategic ones.

Looking ahead, I would expect that pattern to continue, and possibly tilt even further toward financial deals. As capital looks for disciplined growth opportunities in a stabilizing market, investment firms may see more upside in backing strong independent brands rather than consolidating them outright.

The importance of brand

In line with many of the trends I have written about previously, 100 percent of the industry executives interviewed for the study agreed that brand strength will become more important moving forward.

That may sound obvious from a consumer perspective. But in M&A, a strong brand has not always been a prerequisite.

For private equity firms, a company with solid financials but limited brand equity can actually be appealing. If the fundamentals are sound, investors can acquire the business at a more attractive valuation and create value by upgrading marketing, refining positioning, and expanding distribution. In that scenario, weaker brand recognition can mean a lower entry price and more room for multiple expansion.

If well established brands become table stakes for deals, that changes the equation. Private equity investors would need to pay a premium upfront for companies that already command pricing power and customer loyalty.

Keys to growth

Houlihan Lokey identified several themes expected to drive future M&A activity. While the report outlined multiple factors, these stand out as particularly important:

Presence in, or the ability to produce, e bikes

Strong and defensible branding

Vertical integration, especially with direct to consumer distribution

Streamlined production models with healthy margins

As the industry stabilizes, brands are positioning themselves to grow again. If forecasts hold, the next few years could bring another surge in M&A activity.

My suspicion is that there will be a lot more smaller deals that might necessarily create big headlings. These acquisitions could strengthen balance sheets, improve operations, and ultimately benefit founders, investors, and consumers alike.

Back to the M&A stigma

I alluded to it earlier, but the elephant in the room is how cycling fans feel about outside capital entering the brands they love.

Many will point to Rapha and argue that external investment contributed to the erosion of what was once a dominant and culturally defining brand. There is some truth to that critique. At the same time, it is far too simple to say outside money automatically leads to brand decline. There are plenty of examples that complicate that narrative.

Take ENVE Composites. The Utah based carbon wheel and component manufacturer has gone through two acquisitions in the past decade. In 2016, it was acquired by Amer Sports for 50 million dollars. In 2024, it was sold again to PV3 Investments for an undisclosed amount.

An undisclosed sale price often raises eyebrows. In some cases, that language can mask underwhelming returns. It is reasonable to assume that may have been part of the story here. According to PitchBook data, ENVE’s annual revenue reportedly grew by only about 4 million dollars between 2016 and 2025. That is essentially flat growth over nearly a decade, suggesting Amer Sports likely did not see the kind of return it hoped for.

But that does not mean private ownership was inherently bad for the brand.

Under Amer Sports, ENVE remained highly regarded in the market. Its wheels are used by UAE Team Emirates, one of the most successful road teams in modern history. The company also expanded into complete bikes, which have been widely praised for their design and ride quality. The fundamentals of the brand remained intact.

It is also worth noting that the owner of PV3 Investments is an avid cyclist. That alignment of passion and capital, combined with ENVE’s stable positioning at the premium end of the market, could create a more focused growth chapter.

Strategic acquisitions tend to face less backlash from consumers. In many ways, they are simply part of the industry’s fabric. One of the most prolific strategic acquirers is SRAM, which has built a portfolio that includes:

RockShox

Velocio

Zipp

Time

Quarq

Hammerhead

SRAM certainly has its critics, but rarely because it acquires brands. If anything, its track record shows that strategic consolidation, when executed thoughtfully, can strengthen innovation, distribution, and brand longevity.

Outside capital is not inherently good or bad. The outcome depends on structure, incentives, leadership, and how well the acquiring party understands the culture of the brand they are backing.

Finding brands on the verge

Up to this point, everything I have outlined is informed speculation based on the data available to us. We do not know whether increased M&A activity will materialize, or how it would ultimately reshape the industry.

That said, my hypothesis is straightforward. The cycling industry is filled with small to mid sized brands that present attractive targets for private equity investors and strategic buyers alike.

Most headline deals will likely focus on brands serving the broader mass market. But within the performance and enthusiast segment, there are companies that could generate respectable returns on a shorter investment horizon, think three years rather than seven to ten. Smaller funds, especially those with genuine ties to cycling, may view these brands as relatively safe, brand driven growth plays.

For founders and operators, the appeal is just as clear. Outside capital can provide operational guidance, expanded distribution, marketing resources, and supply chain leverage that meaningfully accelerate growth. There are risks to that strategy, and I will address those shortly. For now, it is worth highlighting a few brands that strike me as compelling investment candidates.

Pas Normal Studios

This is not the first time I have written about Pas Normal Studios in Built on Bikes. The Copenhagen based apparel brand has consistently outperformed larger competitors in the premium cycling category. Its disciplined growth strategy and sharp brand identity have positioned it as one of the most influential players in modern cycling apparel.

With reported 2024 revenues of approximately 27 million dollars, the company is substantial, but still meaningfully smaller than a brand like Rapha. That makes it large enough to matter, yet small enough to grow.

There is also a structural nuance worth noting. One of the founders previously launched Wood Wood, a respected name in luxury streetwear. That background matters. In luxury fashion, M&A activity is common, and founders are often familiar with minority stakes, growth capital, and strategic partnerships.

In fact, Pas Normal Studios already has outside investment. Archive Srl, the investment vehicle of the family behind Moncler, holds a minority stake in the company. That existing structure suggests two things. First, the founders are comfortable operating with outside capital. Second, there is already institutional validation of the brand’s long term value.

Pas Normal has already ventured into off-the-bike clothing that appeals to luxury fashion and streetwear consumers beyond cycling, making them an attractive acquisition target for PE firms already investing in the fashion industry. With experienced founders at the helm, Pas Normal could navigate an acquisition strategically and potentially challenge Rapha’s market position.

Ventum

Another brand you might recognize from a previous story is the bike manufacturer, Ventum. This brand shares many qualities with an earlier version of Canyon with their sleek race designs and a direct-to-consumer model. But Ventum hasn’t expanded as rapidly, and I don’t think that should even be the goal.

Ventum excels at making affordable frames with an emphasis on race geometries for triathlon, road, and gravel. Their consolidated frame selection shields them from the excess inventory problems that have plagued brands like Canyon and Trek.

Two resources that would unlock Ventum’s next phase are better distribution in the EU and Asia, plus expanded manufacturing capabilities to meet rising demand. Otherwise, Ventum is already operating with efficiency, scalability, and healthy margins.

A strategic acquirer is hard to envision, but a PE firm with bike industry experience could provide the capital and infrastructure to elevate Ventum to the level of Pinarello or Factor while maintaining their price advantage.

Wolf Tooth Components

Wolf Tooth Components specializes in making high-quality bike components and accessories. Within the performance and equipment-focused communities, the brand has made a name for itself by producing components that can significantly upgrade the efficiency or functionality of certain parts of a bike.

Based out of Minnesota, the brand is already producing a large volume of products, indicating they have formed an incredibly efficient base of operations. Wolf Tooth has a strong direct-to-consumer business but also maintains a healthy retail footprint in the United States through their ecosystem of partner dealers.

The brand’s next step is major retail expansion, specifically in markets outside of the United States. For this goal, a strategic acquisition from a major retailer could make sense. Decathlon could be that acquirer.

Decathlon is the largest global retailer of outdoor equipment in the world, with thousands of stores spread across 60 countries. With annual revenues reaching 15 billion euros, Decathlon is positioned to easily acquire smaller brands.

The move wouldn’t be to acquire Wolf Tooth for exclusive retail rights but rather to increase traffic and sales in their bike department, which is on the rise. Decathlon recently introduced its in-house bike brand Van Rysel, and demand has been exceptional. Acquiring Wolf Tooth could offer an easy upsell on new Van Rysel purchases and make Decathlon a go-to destination for bike enthusiasts seeking quality parts faster.

Cycling will need money in the post COVID era

Whether we like it or not, the cycling industry will need more investment in a post-COVID world if we want the sport and the activity to continue growing. I don’t think the goal should be to return to pre-COVID M&A numbers. Increased investment from outside investors will certainly hurt the quality of certain brands, but it will also benefit deserving brands that will eventually reward consumers with better products.

Just like when I talk about funding development in the United States, the best-case scenario for financial investment is the presence of people who care about cycling and have experience investing in consumer brands in a growth capacity. All we can do is keep our eye on where the money goes over the next few years.

Ride and rip,

Kyle Dawes