Rapha's Bet on the United States

Does the brand's new focus on American cycling represent real opportunity in the market?

In an early edition of Built on Bikes, I examined how Pas Normal Studios has taken a steady, disciplined approach to brand growth. I contrasted that strategy with the increasingly erratic financial performance of Rapha, a legacy brand in the premium cycling apparel space that has been on a downward trajectory for several years. I still stand by my conclusion from that piece. Rapha needed to take decisive action to stabilize the business. It appears the leadership at Rapha agreed.

Since that article was published, Rapha has made a series of moves that suggest a far more aggressive and unsentimental approach to regaining its position at the top of the premium apparel market. In the months that followed, the brand has:

Closed five global clubhouses that function as retail locations, four of them in the United States

Ended its long standing sponsorship of both the men’s and women’s EF Education WorldTour teams

In an interview with BikeRadar, newly appointed CEO Fran Millar noted that the United States currently accounts for roughly 20 percent of Rapha’s global business. Rapha remains the largest brand in the premium cycling apparel category, but the rise of competitors like MAAP, Pas Normal Studios, and Velocio has forced the company to confront several years of weak financial performance and slowing momentum.

That is what makes the renewed focus on the United States so interesting. If the U.S. represents only one fifth of Rapha’s revenue, why double down here instead of refocusing on Europe or accelerating growth in emerging markets like Asia? At the same time, the closure of four U.S. Rapha clubhouses creates the impression that Rapha is pulling back from the American market rather than investing further into it.

This piece is not an attempt to judge whether each individual decision Rapha has made is correct. Frankly, that question isn’t that interesting to me. What I am more interested in is whether this strategic shift toward the United States reflects a genuine growth opportunity for cycling domestically, or whether it represents another risky bet by a brand under pressure. If Rapha is right, it may signal untapped potential in the U.S. cycling market. If they are wrong, it could reinforce the idea that meaningful growth here remains elusive.

Why look at Rapha?

As always, I’ll caveat this by saying that everything here is my opinion, and I could be completely wrong. This question is a difficult one to answer. Can the strategic pivot of a single company really tell us anything meaningful about the potential of the U.S. cycling market? The honest answer is yes and no.

Viewed narrowly, Rapha is just one data point. But it is an important one. Rapha remains one of the largest apparel brands in cycling and, since its acquisition by the Walton family, has become more deeply embedded in the American cycling ecosystem. That context matters.

It is not surprising to see smaller, high-growth brands like Pas Normal Studios and MAAP investing heavily in the United States. They are a fraction of Rapha’s size, and the U.S. is the largest consumer market in the world. For emerging brands, that represents a significant opportunity to capture and steal market share.

Rapha’s situation is fundamentally different. As a much larger company facing real financial pressure, its strategic decisions are unlikely to be made lightly or opportunistically. If the goal is a return to sustainable growth, Rapha will need meaningful momentum to reverse several years of underperformance. A substantial bet on the United States suggests the company believes there is upside here that is not immediately obvious to the average consumer.

Only time will tell whether that belief proves correct. For the purposes of this piece, however, Rapha provides a unique and useful lens through which to examine the current state and potential of the American cycling market.

How do we determine if the hype is real?

If we are going to use Rapha as a lens into the wider U.S. market, then it becomes critical to understand how and why these strategic decisions are being made. What are Rapha’s executives seeing in the United States? Is this a targeted push to stabilize the business, or a broader bet that the U.S. cycling market is on the verge of explosive growth? The answer to that question will tell us far more about market signals than any single press quote ever could.

How do we gain insight into Rapha’s decision making process beyond what its CEO has said in interviews? Simple, we will have to think like a strategy consultant.

This approach goes against much of what I have historically argued for when it comes to growing cycling in the United States. I have always emphasized storytelling, cultural investment, and long term foundation building. Strategy consulting firms, on the other hand, are known for prioritizing numbers, operational efficiency, and profitability above all else. Identify bad business practices, cut unprofitable initiatives, and reallocate resources toward activities that move the balance sheet in the right direction.

Viewed through that lens, Rapha’s recent decisions begin to make more sense. The initiatives being cut are the same ones that have traditionally carried the brand’s storytelling and cultural weight. That tradeoff aligns closely with a classic consulting mindset. It is entirely plausible that Rapha has either hired a strategy consulting firm or adopted a similar internal framework to restructure its operations and reset expectations.

To be clear, I do not like seeing Rapha clubhouses close or storytelling platforms disappear. There is real cultural loss in those decisions. But there is also an argument that this kind of blunt, black and white approach is an attempt to rebuild the foundations of the business. Stability has to come before new ambitions.

If Rapha is able to regain financial footing and return to sustainable growth, there is every reason to believe the storytelling that helped define the brand will return, and potentially with even greater impact. We may not like the approach in the moment, but the hope is that it pays dividends over the long term.

Thinking like a consultant

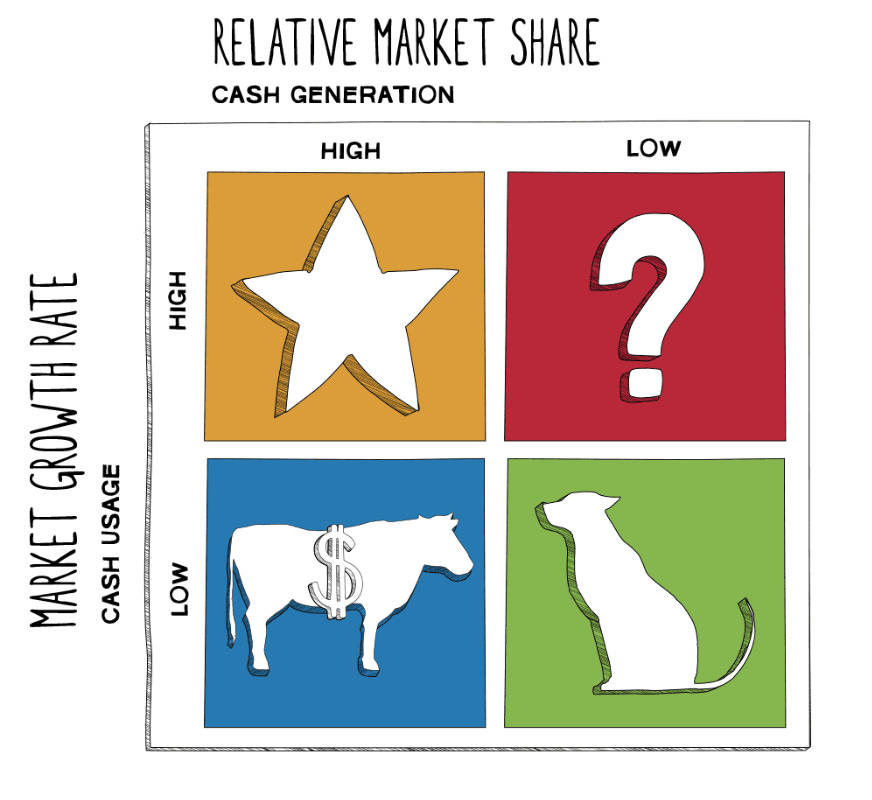

I’m not a strategy consultant, but there are well-established consulting frameworks we can use to try to make sense of Rapha’s recent decision making. One of the most widely used is the BCG Matrix, developed by the Boston Consulting Group.

At its core, the BCG Matrix is a simple way to break down a company’s operations and evaluate where capital, attention, and resources should be allocated to improve financial and operational performance. It maps products or business units across two variables: market share and market growth. Together, those variables create four quadrants that categorize how different parts of a business contribute to its overall health.

Dogs:

Low market share in low-growth markets. These are often the products or initiatives that get cut in order to free up capital and reduce operational drag.

Question Marks:

Low market share in high-growth markets. These areas require heavy investment and carry risk. With the right execution they can become Stars, but without it they often slide into Dogs.

Cash Cows:

High market share in low-growth markets. These businesses generate more cash than they consume and often fund experimentation or growth elsewhere in the company.

Stars:

High market share in high-growth markets. They are expensive to maintain but, if growth continues, can eventually mature into Cash Cows.

Using this framework, we can attempt to place Rapha’s key operations and strategic initiatives into the matrix and better understand the logic behind recent cuts, investments, and shifts in focus. Once that picture comes into view, we can begin to extrapolate what Rapha’s leadership may be seeing in the U.S. market and whether their strategy reflects genuine opportunity or calculated necessity.

The Dogs

If we are going to examine the weakest links in Rapha’s business model, there are two areas that stand out as high cost and low reward.

Clubhouses

Clubhouses became a core part of Rapha’s identity and were pioneers in using community engagement to grow cycling and establish deep brand loyalty. It is undeniable that clubhouses played a critical role in Rapha’s early growth in the United States, particularly through the RCC membership program. They gave cyclists a physical space to gather, ride, and connect, while also serving as premium retail locations. Over time, they evolved into a global network that RCC members could rely on when traveling or shopping, reinforcing Rapha’s position as more than just an apparel brand.

As the cycling landscape has evolved, however, it appears that at least in the United States some clubhouses have begun to deliver diminishing returns, both financially and culturally. Much like the rise of run clubs, platforms like Strava have made it easy for anyone to organize group rides and build communities without the need for a centralized brand hub. In most major metropolitan areas where Rapha clubhouses exist, riders now have an abundance of group rides, events, and social scenes to choose from. Rapha no longer controls the narrative or infrastructure around physical community building in the way it once did.

At the same time, clubhouses are retail locations at their core. In the U.S., they are concentrated in cities with extremely high real estate costs and rising labor expenses. In the early days, those costs could be justified by the outsized marketing impact and cultural relevance the clubhouses delivered. As the market has become more saturated and community-driven cycling less centralized, it’s unlikely that many of these locations could continue to justify their operating costs on a purely financial basis.

It’s awful that we are losing four clubhouses in the United States. Full stop. That loss will be felt by local cycling communities and longtime Rapha loyalists. That said, shuttering these locations does not necessarily weaken Rapha’s position in the United States. In fact, it may do the opposite. Closing cash intensive clubhouses frees up significant capital that can be redeployed into new initiatives with higher impact, better scalability, and clearer paths to profitability in the U.S. market.

WorldTour affiliation

Rapha’s partnership with the EF Education WorldTour team is another example of an initiative that delivered massive early upside before producing diminishing returns. When the partnership debuted, Rapha was immediately positioned as the brand with the most distinctive kits in the WorldTour. The bold designs and prominent use of pink, aligned perfectly with EF Education’s branding, stood out in a conservative peloton and quickly became a fan favorite.

The partnership reached its peak when Rapha and EF Education collaborated with PALACE, the London based skateboarding brand. By introducing streetwear aesthetics into professional cycling kits, Rapha cemented its status as the most culturally relevant apparel sponsor in the WorldTour. The collaboration pushed EF Education into the spotlight, making the team instantly recognizable even as on-road results remained inconsistent.

By 2025, however, the novelty had clearly worn off. What was once disruptive had become normalized. Eye-catching kits alone were no longer enough to drive incremental sales, particularly in mature European markets where Rapha already had strong brand awareness and where overall cycling growth had begun to plateau. The partnership remained expensive, but the marginal returns appeared to be shrinking.

Once again, by cutting this partnership, Rapha will free up significant capital and operational resources that can be reallocated to new endeavors.

Cash Cows

There could certainly be more, but the only true cash cow I can clearly identify is European road cycling apparel. While I just argued that sponsoring a WorldTour team had effectively become a dog, marketing and sales are not the same thing. WorldTour representation may no longer be driving meaningful incremental growth in Europe, but that does not mean demand for Rapha’s road apparel in the region has collapsed or become insignificant.

We know the United States accounts for roughly 20 percent of Rapha’s business. It is reasonable to assume that South America, Africa, and Australia contribute relatively small shares of revenue, even when combined. That narrows the remaining revenue concentration to Europe and Asia. While Asia represents a growing opportunity, Europe remains the region where cycling participation, cultural relevance, and premium apparel adoption are strongest.

Europe is still where Rapha has its deepest brand equity. The company has the recognition, distribution, and credibility to maintain strong sales without the need for aggressive marketing spend or dramatic rebrands of its road collections.

The strategic play, then, is straightforward. Continue executing in Europe, protect market share, and use that steady cash flow to fund higher-risk, higher-upside bets elsewhere. Even as competition intensifies from brands like MAAP, Pas Normal Studios, and Velocio, Rapha’s scale and legacy still allow it to outperform these challengers in absolute revenue.

The risk here is complacency. Without some level of reinvestment, brand erosion in Europe is inevitable over the long term. But in the near to medium term, European road cycling apparel remains Rapha’s financial foundation, providing the stability required to support the broader strategic reset now underway.

Stars

With stars usually being the products or segments that brands focus their attention to spur growth, this section is pretty straightforward and has either been explicitly defined by Rapha or alluded to by recent strategic decisions.

U.S. enthusiast market and off-road disciplines

I want to caveat this segment by acknowledging that this remains a relatively narrow segment within the broader cycling market and one that ties closely to what I will discuss later in the question marks section. That said, the core idea is simple. The population of cycling enthusiasts in the United States, particularly within off road disciplines, represents a strong foothold from which Rapha can expand.

I have written about this extensively in previous editions of Built on Bikes, but off road cycling is currently the most effective channel for converting Americans into committed cyclists. These are people who ride consistently, invest in equipment, follow the sport, and often participate in racing or organized events. It is a developing market that requires meaningful investment to gain visibility and credibility, and while it may not immediately translate into mass volume sales, it is where long term loyalty is being built.

To date, Rapha has not been lagging in this segment. If anything, it has been one of the most visible premium brands in U.S. off road racing. Early signals of this strategy included sponsorships of athletes like Sarah Sturm, Keegan Swenson, and Colin Strickland. That investment only deepened over time with the formation of a dedicated off road team and significant marketing spend behind Lachlan Morton’s endurance projects, which helped redefine what modern cycling storytelling could look like.

More recently, Rapha has continued to reinforce this position through its partnership with USA Cycling, sponsorship of Kate Courtney and the She Sends Foundation, and the signing of Cam Jones, the 2025 Life Time Grand Prix overall winner. These are not reactive moves or attempts to regain relevance. They are the continuation of a long running strategy that has quietly positioned Rapha at the center of elite off road cycling in the United States.

Rapha is not trying to make up lost ground here. While brands like Pas Normal Studios and MAAP may have taken the lead in fashion forward aesthetics, Rapha arguably has deeper and more credible representation within U.S. off road cycling, both among professional athletes and engaged consumers. The brand is already embedded where influence matters most. If Rapha begins reinvesting more aggressively into sponsorship, product development, and targeted marketing within this segment, the upside could be significant. The groundwork has already been laid, and that is what makes this segment so strategically compelling.

Direct-to-consumer E-commerce

This star channel is not exclusive to the United States, but it remains critical to Rapha’s revised strategy for the American market.

Rapha has shuttered several clubhouses in the United States, but that does not mean it will stop selling to the customers who once shopped there. With much of the fixed cost associated with operating physical retail now removed, Rapha has the opportunity to reallocate capital toward strengthening its direct to consumer infrastructure and logistics.

Rather than having marketing dollars tied up in high rent locations in a handful of cities, Rapha can invest more heavily in digital acquisition and retention. Online advertising allows the brand to target cycling enthusiasts across the entire country, not just those within riding distance of a clubhouse. This significantly expands reach while improving efficiency.

At the same time, reinvesting in e-commerce, fulfillment, and customer experience reduces friction for American consumers who already view Rapha as a premium brand but may not have had consistent access to physical stores. If executed well, this shift does not weaken Rapha’s presence in the United States. It modernizes it

Question Marks

This is where the real question mark of this article comes from. There are two big question marks for Rapha in their new strategy.

The broader U.S. cycling market

The broader American cycling market, beyond core enthusiasts, does not currently have a dominant apparel player. Once you look past people who view cycling as a serious form of exercise or competition, the majority of riders in the U.S. are commuters. That market is already being addressed successfully by e bike brands, helmet manufacturers, and accessories companies. Dedicated cycling apparel, however, has largely failed to penetrate it.

The reason is simple. Most Americans who use a bike as transportation are riding short distances and do not want to change clothes when they arrive. They wear normal street or work clothing, not performance oriented cycling kits. From the outside, it appears the apparel industry has either failed to crack this use case or has decided the margins are not worth the effort.

From a BCG Matrix perspective, this is where the risk becomes clear. Rapha’s lifestyle collections currently trail far behind its performance apparel in both sales and adoption. In today’s state, that category looks like a dog rather than a star. Pursuing the commuter and lifestyle market at scale would therefore require meaningful investment into a segment that has not yet proven it can drive growth for the brand.

Olympic and national partnerships

With their new focus on the United States, one of the most significant moves by Rapha was becoming the official apparel partner of USA Cycling. I’ve seen mixed reviews of the partnership, but it is far too soon to pass judgment because we don’t know the exact strategic reasoning behind the decision.

We know Rapha is prioritizing the United States, but who is this partnership actually targeting? It’s reasonable to assume that the 2028 Olympic Games in Los Angeles play a role. Rapha, a British company, is likely hoping for a similar effect to what the 2012 London Olympics had on British cycling. After strong performances by the national team, Britain saw a noticeable increase in cycling participation and enthusiasm. Rapha didn’t supply Team GB’s kits at the time, but it’s hard to imagine that a similar moment in the U.S. wouldn’t result in a meaningful sales boost if they were.

I’m almost certain this is the question mark Rapha believes could become a star.

Framing the matrix

Overall, Rapha has plenty to work with as it begins its new American-focused strategy. It appears the company has already identified two major dogs in the business and eliminated them to free up significant capital to reinvest in stars and question marks. It is slightly concerning that there is only one major cash cow, but it is also the foundation on which Rapha’s entire empire is built. In the near term, it feels like a reliable base that should not require significant resources to continue generating steady revenue.

Rapha has also identified a clear star in the American enthusiast and off-road markets and has been investing in these segments for years. The brand is now well positioned to turn this star into a smaller but still meaningful cash cow. Finally, two major question marks loom over Rapha’s new strategy, bringing us back to the core question: does Rapha’s investment in the American enthusiast market represent a real opportunity to grow cycling in the United States?

Opportunity comes in all shapes and sizes

With all of that analysis behind us, I think I’m able to answer my overarching question about growth opportunities in American cycling. Rapha’s investment in the United States does signal a real opportunity to grow cycling domestically, but it falls short of a full cultural revolution. Ultimately, I think Rapha is focused on growing and reclaiming dominance among cycling enthusiasts.

I highly doubt the Olympics will spur more towns and cities to adopt bike-forward policies like Bentonville, Arkansas, but I do think it could result in the largest cultural shift in American cycling to date. It’s a narrower market, but with off-road and adventure-based cycling firmly on the rise in the United States, the Olympics could push more people to research cycling as a serious hobby. That, in turn, would lead them to discover entry points into these popular disciplines that Rapha is actively targeting. If those consumers have already seen Rapha on their screens being used by top athletes, trust will already be built in Rapha as a go-to brand.

It’s a long-term play, but if Rapha is able to reclaim its position as the dominant performance- and culture-driven brand it once was, this time rooted in the United States and alternative cycling disciplines, I think it will have created the foothold necessary to eventually break into the wider U.S. consumer market.

From a business perspective, this is the strongest Rapha has looked in years in terms of having a clear, concrete strategy to return to success. Out of all the markets and channels they could have pursued for growth, they chose the United States and alternative, emerging cycling disciplines as their primary focus.

I’m fully aware of my own bias given my desire to see professional cycling grow in the United States, but I do think Rapha’s reorganization lends real credibility to the idea that meaningful professional growth here is possible.

Ride and rip,

Kyle Dawes

I liked this, and I spend a lot of time thinking about Rapha. I often think a large part of Rapha's downfall was that it moved away from its core market. Simon Mottram is a branding genius and a cycling geek. He built Rapha for people like himself. Since he sold the business, Rapha seems to be lost. They now have a limited foothold in the road conversation (especially with the new generation), and they're going after a new (smaller) market in off-road. I can't help but think the big off-road push in the US is just as much to appease its owners, as it is sensical.

Good article. My view is that their biggest issue is the product they are selling. Nothing has changed in their designs, same stripe, same colours for the most part. I don’t want a kit from 10+ years ago.

Smaller companies have fresh designs that just look better.

Do they need core, brevet, race team, etc. I think their product lines could be streamlined and simplified.

Another issue is the regular 40% off sales. Who buys their kit at full price?

Quality also seems to be slipping.

I may sound negative. I am not, more sad than anything. I do want a want them to succeed but in my view it needs to start with a product that people want to buy, not the same product that Simon came up with in 2004/5