The High-End Nutrition War Nobody Is Watching

Maurten is rising, Science in Sport is restructuring, and private money is fueling both sides of a collision course for premium endurance nutrition dominance.

Built on Bikes is a cycling publication at its core and always will be, but occasionally I like to touch on adjacent topics that are particularly compelling. High-performance endurance nutrition is one of those areas. It is something I have obsessed over throughout my cycling career, spending years researching, purchasing, and working through a seemingly endless market of brands. I still have not landed on a perfect formula, but I have figured out the brands I trust.

I fall firmly in the snob category. I bias toward high-end, high-carb brands like Maurten, Science in Sport (SIS), Carbs Fuel, MNSTRY, and Neversecond. Based on perception alone, each brand carries a distinct identity. Maurten is the minimal, futuristic brand redefining what endurance nutrition looks like. Science in Sport is the original legacy player that helped establish the high-end segment. And newcomers like Carbs Fuel are making a name for themselves by offering comparable quality at a lower price point.

Beyond those five there are dozens of brands venturing into the high-carb era looking to challenge those at the top. On the surface it looks like a saturated market with several brands on similar trajectories. But when I looked closely at the finances of the most prominent premium brands, something stood out. There is a compelling competition playing out between two brands that most consumers, myself included, never think about because it is all happening in the private markets.

That competition is between the incumbent giant Science in Sport and the rising star Maurten. Their financial and strategic positions are almost mirror images of each other, and after analyzing both in depth, I believe they are on a collision course for market dominance. This week I want to look at both brands, their financial and strategic histories, compare where they stand today, and explore what it could mean for the future of premium endurance nutrition. First, it helps to understand each brand and their financial journeys.

Maurten is simple but effective

Founded in 2015 in Sweden, Maurten has become a staple in the endurance sports community. Minimally branded, flavorless, and packed with carbohydrates, they cut out the fluff and deliver on performance through their hydrogel technology, which allows athletes to digest high doses of carbohydrates more easily. Maurten’s growth has been driven largely by elite athlete adoption, with stars like Eliud Kipchoge and Demi Vollering among their most prominent ambassadors.

One moment put Maurten firmly on my radar as a brand operating at a different level than its competitors: a $21.6 million venture capital round in 2024 led by IRIS Ventures. The investment came nearly ten years into the brand’s existence, but that timeline actually reinforces market potential. Maurten did not need outside capital to survive. They raised it to scale. And at a moment when most of their competitors have never seen a significant institutional round, $21.6M is a statement about where this brand is headed.

Since Maurten is incorporated in Sweden, their financial statements are publicly accessible despite the company being privately held. When you dig into those numbers, you begin to understand both why IRIS Ventures invested and what the size of that investment actually signals.

Maurten’s financials: 2017-2024

Maurten’s path to a $21.6M venture capital raise can be broken down into four key storylines: compelling revenue growth, a turn to profitability, efficient cost structuring and operating leverage, and a consistently lean balance sheet.

Revenue Growth

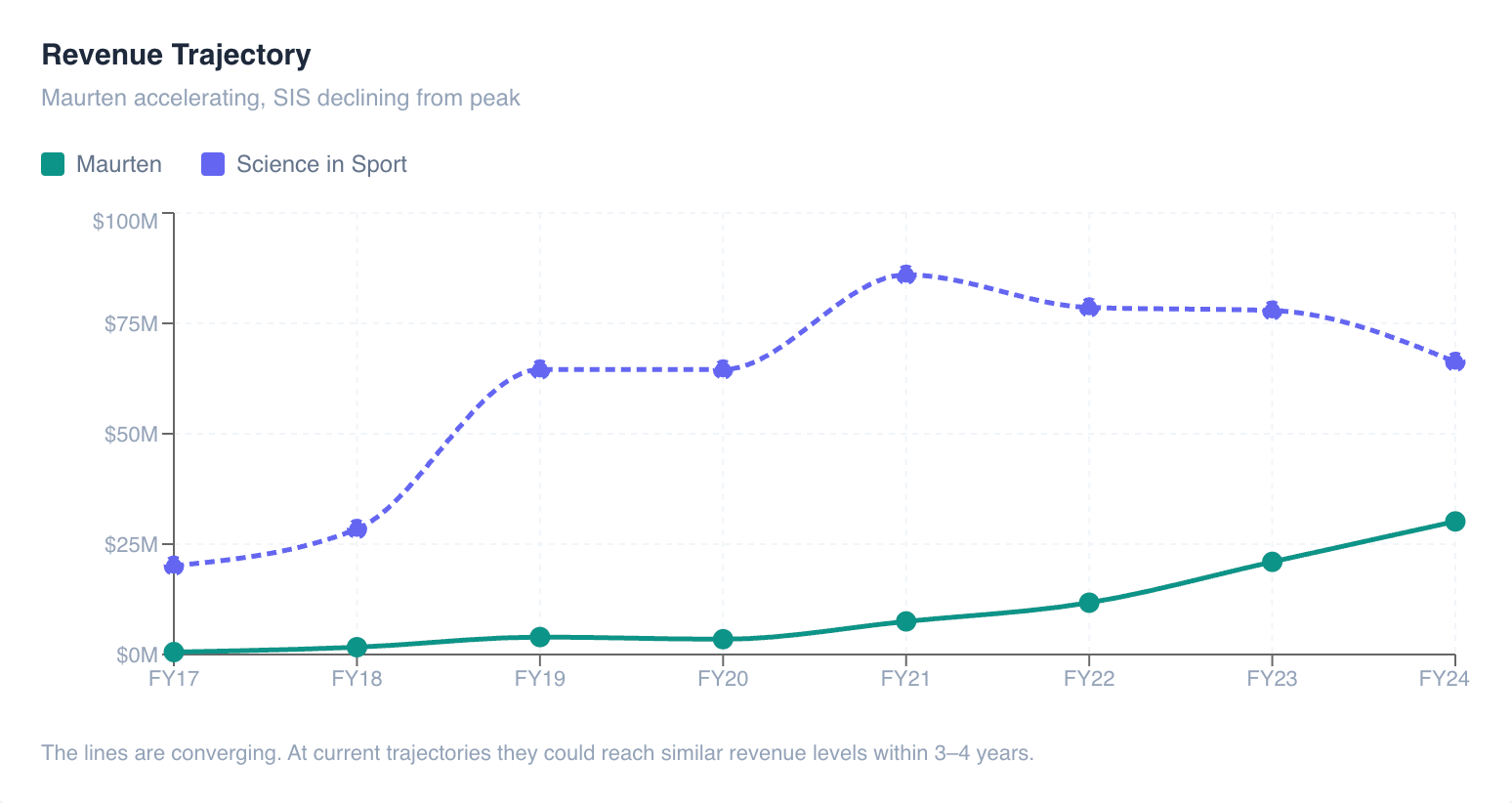

Maurten grew from $553K in revenue in 2017 to $30.1M in 2024. That is almost a 54x increase in seven years. The only down year was 2020, and that was almost certainly due to COVID wiping out mass participation events.

Recent growth rates continue the compelling story:

2022: +85%

2023: +87%

2024: +43%

The deceleration from 87% to 43% might raise eyebrows, but it makes sense. Growing 43% on a $30M base is considerably harder than growing 87% on a $12M base. The trajectory remains strong.

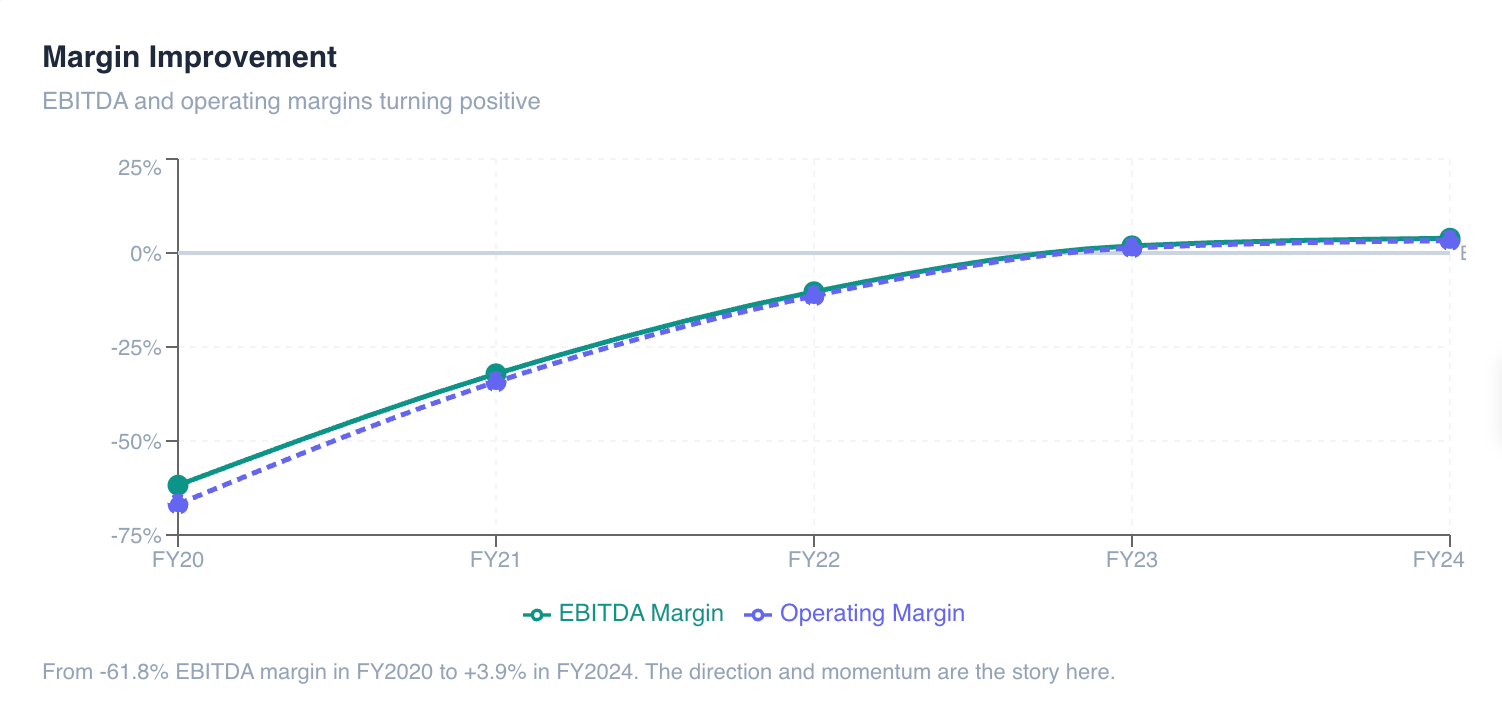

Profitability

Scaling a small CPG business often requires cash burn upfront and that was certainly the case for Maurten. Their burn rate even seemed critical at times, including 2021 when the company lost $2.6M on $7.5M in revenue which equated to a -34% operating margin. Then something shifted:

2022: Still losing money, but losses narrowing sharply to (-$1.34M)

2023: First year of operating profit, $275K

2024: Operating profit nearly quadruples to $991K equating to a margin of 3.3%

2024 also saw the company record its first ever positive net income at $300K. An EBITDA growth rate of 196% and EBIT growth of 258% in FY2024 are numbers that may have made IRIS Ventures move.

Operating Leverage

Between 2020 and 2024 revenue grew 770%. Over the same period wages and salaries only grew 200%. Maurten is scaling revenue dramatically faster than it is adding headcount. That is the definition of operating leverage and it is what makes the margin improvement sustainable rather than a one-time event.

Balance Sheet

No long-term debt. Maurten carries zero bank debt. That is impressive for a scaling consumer brand and makes the business significantly less risky from an investor’s perspective.

Asset-light model. The company carries almost no property, plant or equipment, just $398K. They are not building factories. They are building a brand and outsourcing the manufacturing, which keeps capital requirements low and scalability high.

Healthy liquidity. A current ratio of 3.44 means Maurten has more than three dollars of current assets for every dollar of current liabilities. The business is not at risk of running out of cash in the near term.

One flag worth noting. Cash actually dipped slightly from $3.44M in 2023 to $3.26M in 2024 despite being profitable.

Overall, Maurten has built a clean and efficient operation with a clear trajectory toward long-term success, and they did it without needing to raise significant outside capital. That makes 2024 an interesting inflection point. So what does a $21.6M venture capital raise mean for both Maurten and IRIS Ventures at this stage of the company’s development?

The $21.6M VC round

Maurten’s VC deal closed on July 22, 2024 and fits a classic Later Stage VC investment model. Deal multiples paid by IRIS Ventures provide key insights to what they were underwriting. For those unfamiliar with deal multiples, they are simply a way of expressing how much an investor paid for a business relative to that business’s financial performance. They answer the question: for every dollar of revenue, profit, or earnings this company generates, how many dollars did the investor pay to own it?

Deal Size / Revenue: 0.72x. At 0.72x IRIS Ventures is essentially paying below book value on a revenue basis, which suggests either significant negotiating leverage, or that Maurten’s path to meaningful profitability still carries execution risk in the market’s view.

Deal Size / EBITDA: 18.25x. This is more in line with market norms for a profitable growing business but is not aggressive for a brand with Maurten’s growth profile.

Deal Size / Net Income: 72x. This seems high but makes sense given Maurten’s net income of only $300K on a $30M revenue base. As margins expand this multiple compresses rapidly, which is precisely the return thesis IRIS Ventures is likely underwriting.

The overall picture is of a deal priced conservatively relative to growth, suggesting IRIS Ventures saw an opportunity to buy into a brand at an inflection point before the market fully repriced the profitability story. The capital will most likely be directed toward geographic expansion, continued R&D, and higher profile sponsorships. As I will get into shortly, it is clear that Maurten has ambitions to grow into a brand that competes at the scale of SIS.

Science in Sport, the industry giant

Founded in 1992 in the UK, Science in Sport is one of the original science-backed sports nutrition brands. The brand followed a similar early growth trajectory to Maurten but took the significant step of going public in 2013. Over the years SIS has built a strong reputation through partnerships with some of the UK’s highest performing sports programs, including Tottenham Hotspur, Ineos Grenadiers, and the British Rowing team. It is worth noting that Ineos recently made the switch to Maurten, which says something about the shifting dynamics at the elite level.

Since going public the brand has experienced a trajectory that looks almost like the inverse of Maurten’s, ultimately leading to its acquisition by BD Capital in 2025. That acquisition carries significant implications for where SIS goes from here, so before comparing the two brands directly it is important to understand the financial story and the possible paths forward.

Science in Sport’s financials: 2017-2024

It is worth noting that SIS is a significantly older and larger business than Maurten, and the financials should be read in that context. That said, the same four pillars that shaped Maurten’s story apply equally here: revenue trajectory, profitability trends, balance sheet composition, and operating strength.

Revenue Growth

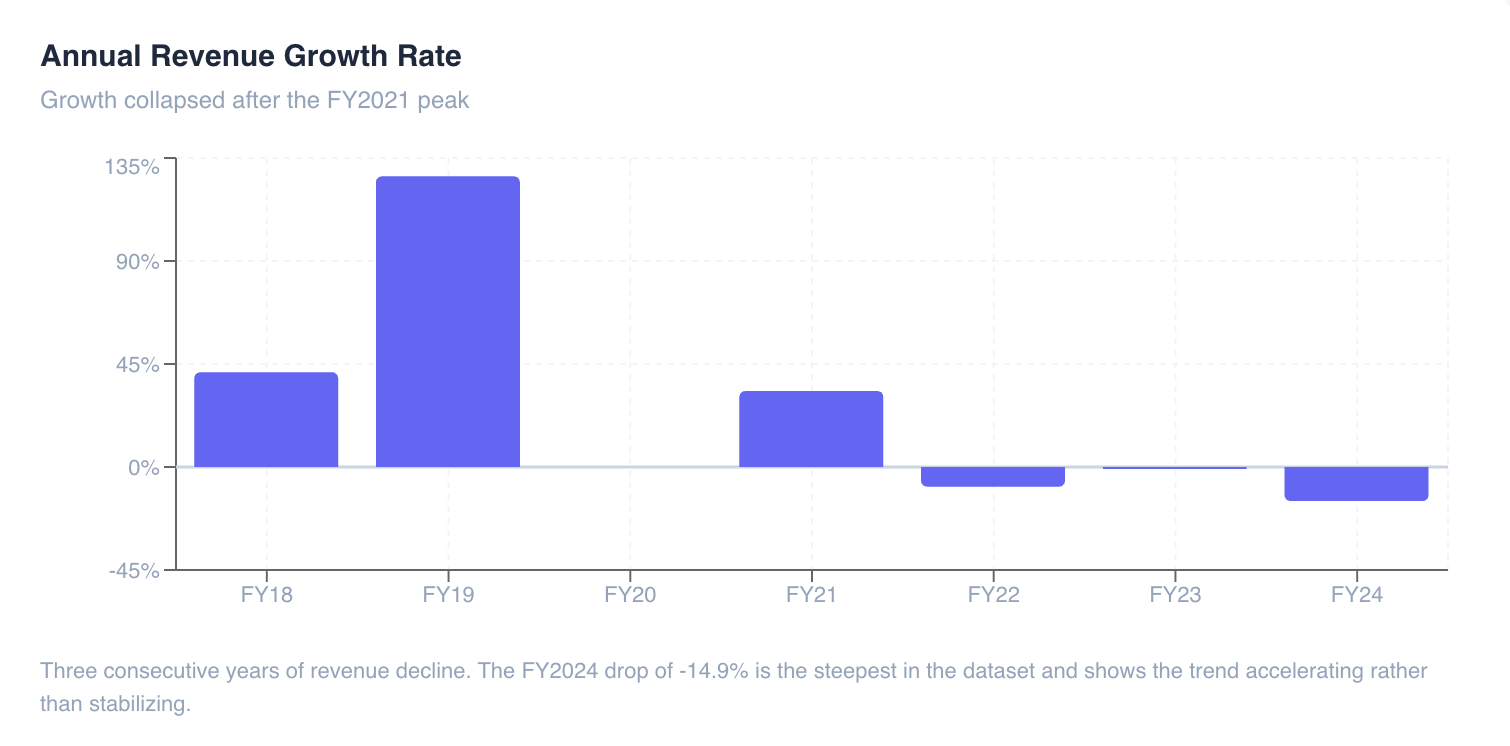

Between FY2017 and FY2024, SIS experienced both significant growth and a prolonged decline. Revenue peaked at $86M in FY2021 before entering a sustained contraction that has continued through FY2024.

2021: $86.0M

2022: $78.6M (-8.6%)

2023: $77.9M (-0.9%)

2024: $66.3M (-14.9%)

While SIS grew revenue 328% from $20.2M in FY2017 to $86M in FY2021, it is important to note that the brand acquired supplement nutrition brand PhD Nutrition in 2018. That distinction matters because acquisition-driven growth inflates revenue without building the underlying brand strength needed to sustain it.

Profitability

This is where SIS’s financials begin to explain why the brand ultimately reverted to private ownership. Across the entire eight-year dataset, SIS did not post a single profitable year.

2017: $(4.6M)

2019: $(7.2M)

2021: $(7.6M)

2023: $(14.0M)

2024: $(6.1M)

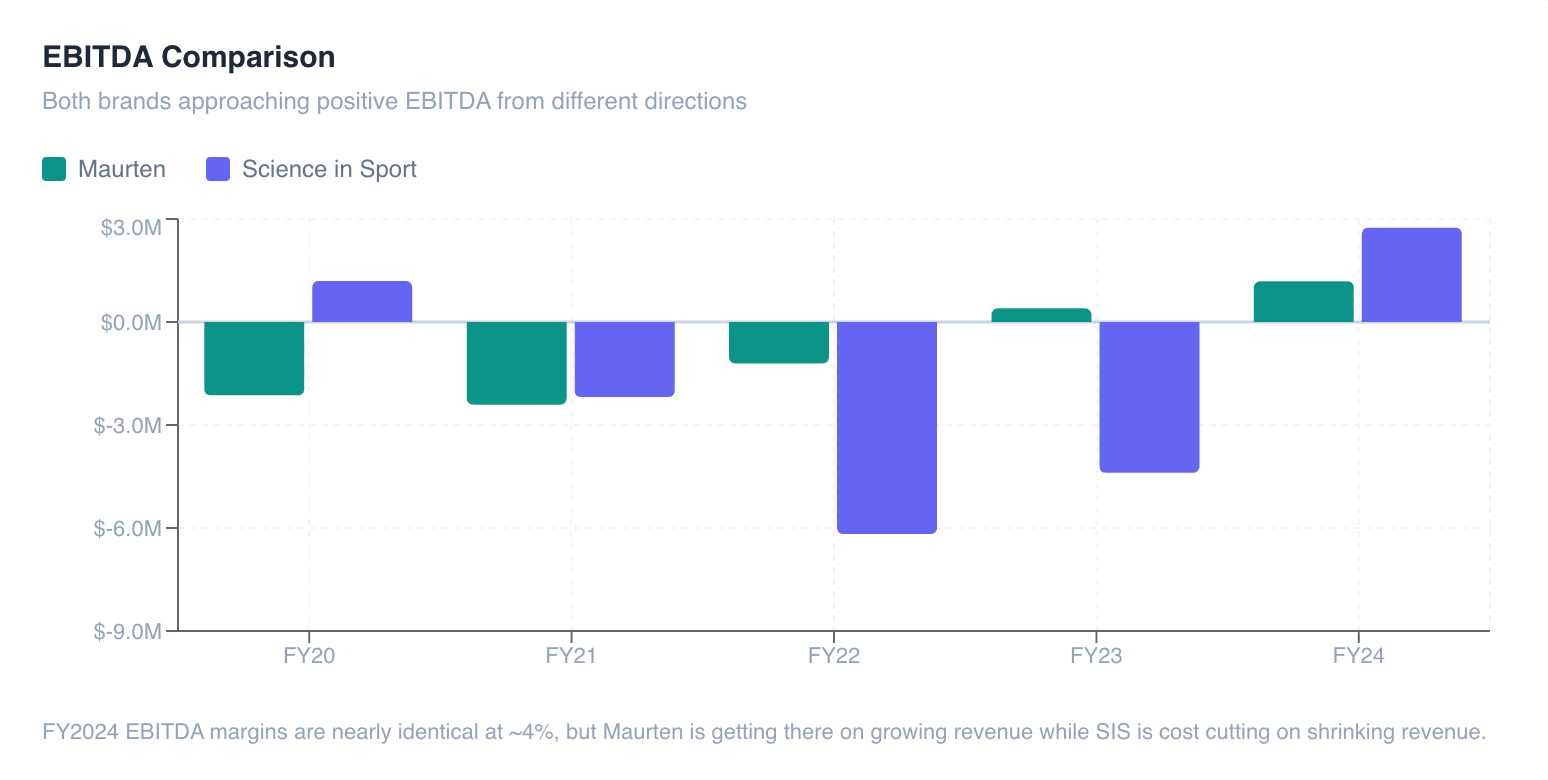

Cumulative net losses across the period total approximately $62.9M. 2024’s reduced loss of $(6.1M) compared to $(14.0M) in FY2023 might look like progress, but it needs to be read in context. The improvement came alongside a 14.9% revenue decline, suggesting the loss reduction was driven more by cost cutting than genuine operating improvement.

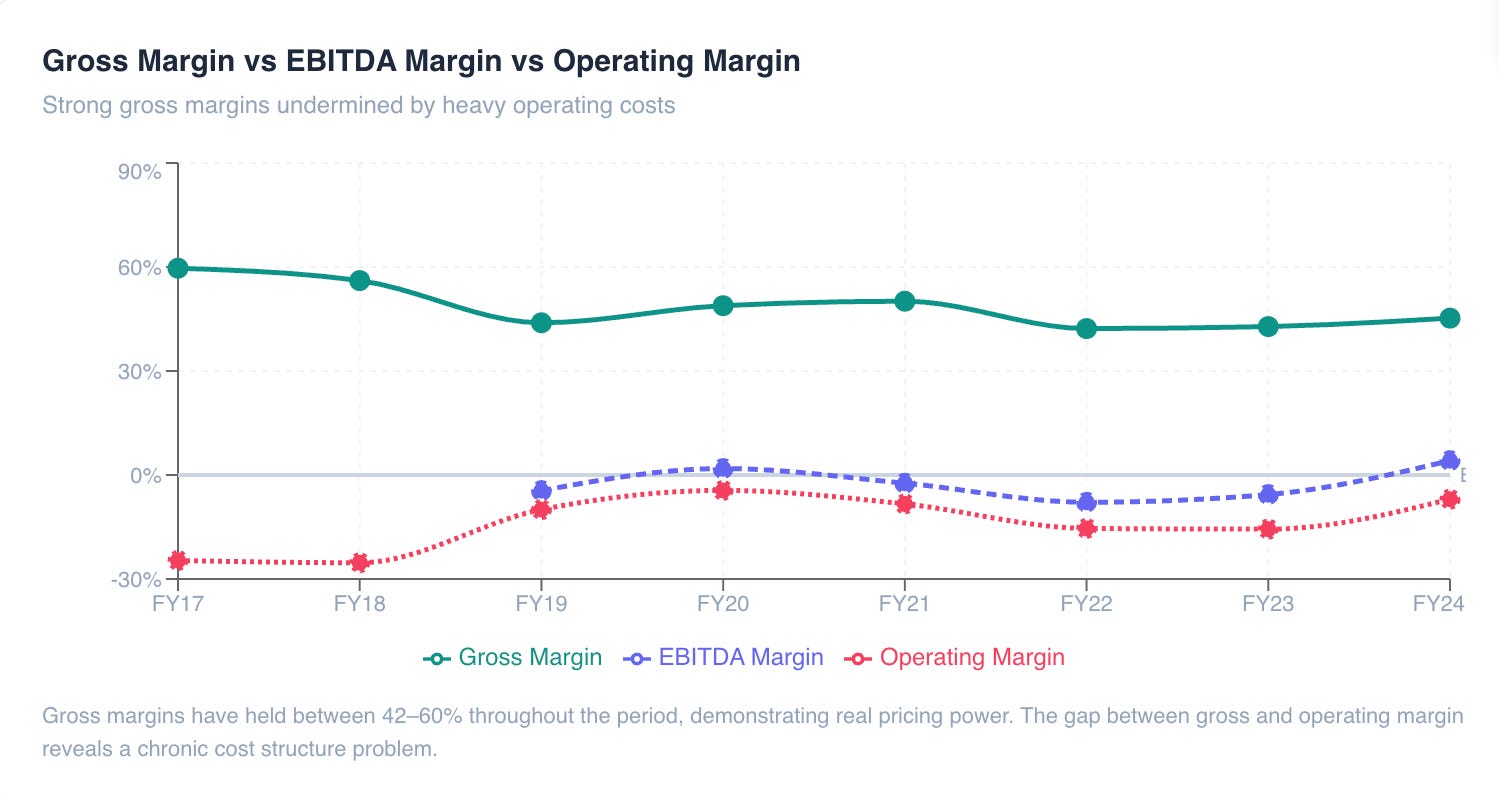

Margins

SIS’s gross margin is the strongest element of the financial profile. At 45.3% in FY2024 it compares favorably to most consumer goods companies. With that said, their operating margin has condensed nearly 14 percentage points from peak to present.

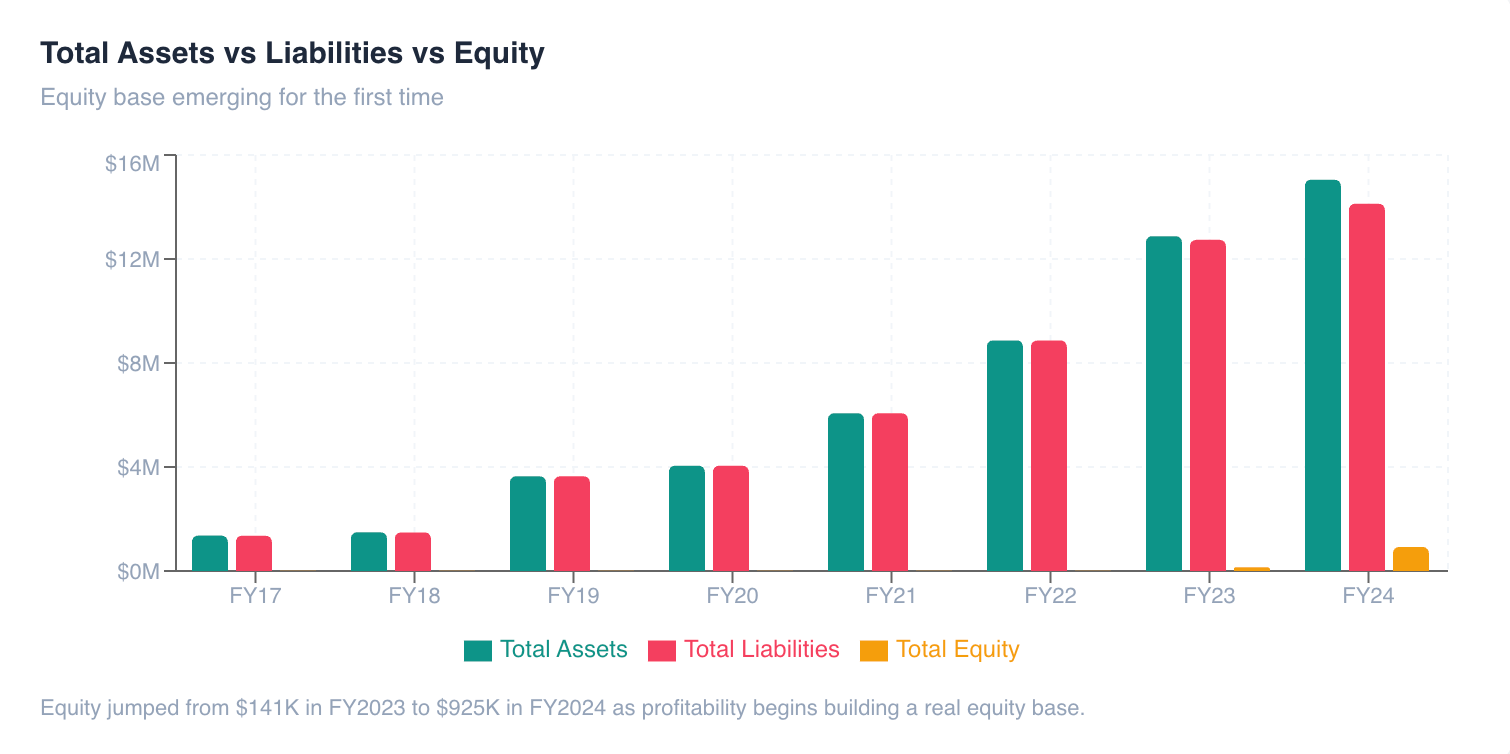

Balance Sheet

Equity is technically positive but fragile. Total equity of $41.2M is supported almost entirely by paid-in capital of $99.8M accumulated through share issuances over the years. Retained earnings are deeply negative at $(57.2M), meaning every dollar of equity is borrowed from shareholders rather than earned through operations.

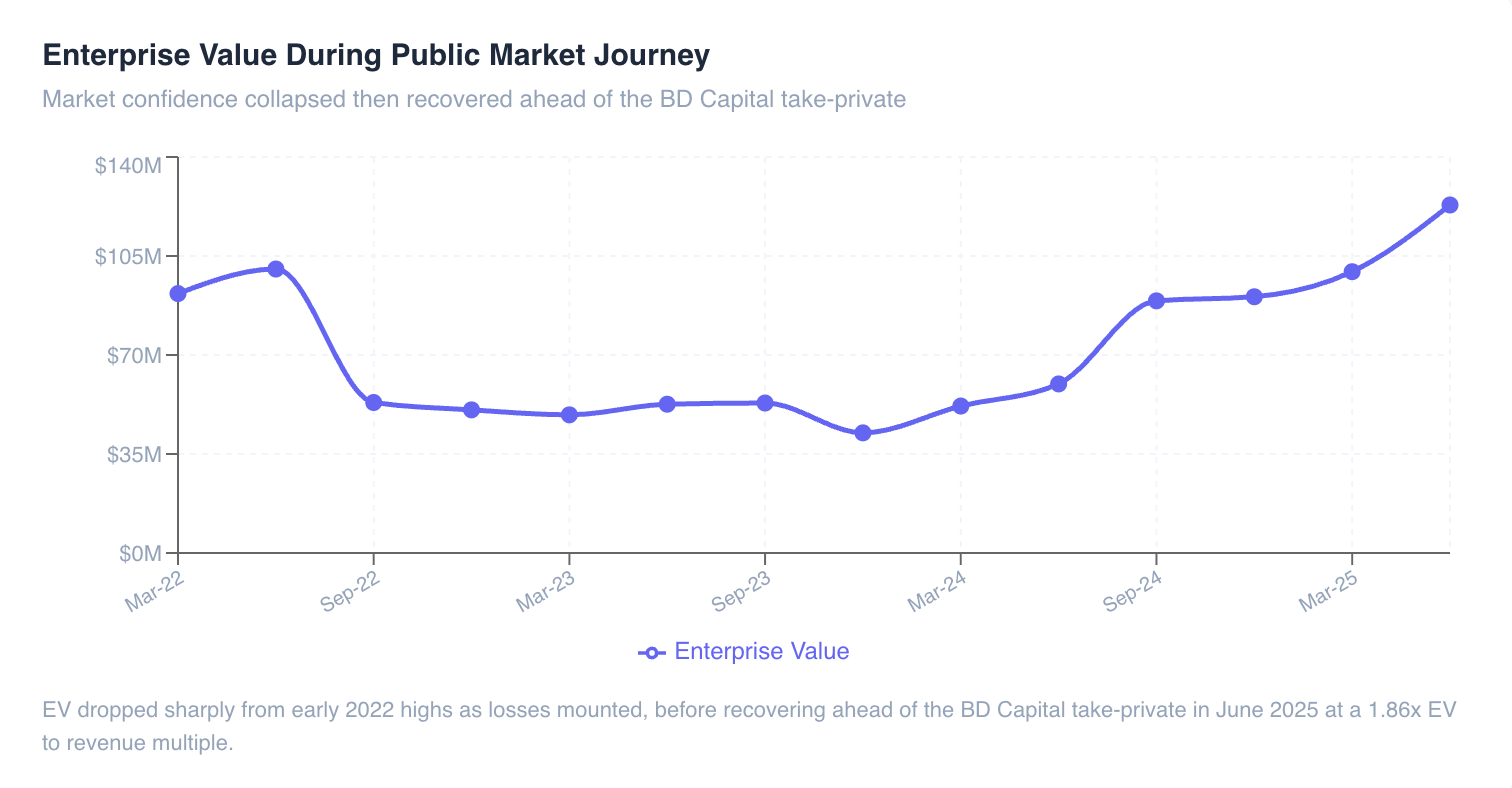

The Altman Z-score of 0.19 is a serious flag. The Altman Z-score is a widely used predictor of financial distress. A score below 1.81 indicates a company in the distress zone. At 0.19 SIS is deep in that territory. This is one of the primary reasons BD Capital took it private. The public markets were pricing in significant financial distress risk and the stock was being punished accordingly.

Debt has appeared and grown. Unlike Maurten which carries zero long-term bank debt, SIS has accumulated financial liabilities. Current financial liabilities of $8.1M and non-current financial liabilities of $12.8M give a total debt position of approximately $20.9M. For a business that is still loss-making this is a meaningful burden.

From public to private

From the numbers it is obvious that SIS was not thriving as a public company, but one of their multiples paints a glimmer of hope. The Enterprise Value to Revenue multiple of 1.86x at delisting compared to 1.22x in March 2022 is interesting. It suggests BD Capital paid a meaningful premium to take the company private, which suggests genuine belief in the turnaround thesis rather than a distressed asset grab.

Maurten vs. Science in Sport

We’ve already laid out the financial story of each company, so this will be a pretty brief recap of the most critical trends when viewing the companies in comparison to one another.

The revenue gap is closing rapidly

SIS is more than twice the size of Maurten on revenue but the gap has been closing rapidly. At SIS’s current trajectory and Maurten’s growth rate they could reach similar revenue levels within three to four years.

Contrast in profitability

Maurten crossed into profitability in 2023 and expanded it in 2024. SIS was profitable on a net income basis across eight years of data. On an EBITDA basis SIS only turned positive in 2024 for the first time.

The EBITDA margins were similar in 2024. Both brands are operating at roughly 4% EBITDA margins, but Maurten is getting there on a growing revenue base while SIS is getting there by cutting costs on a shrinking one. These are fundamentally different businesses even if the margin looks the same.

Maurten is more efficient

Maurten has built a $30M revenue business with $15M in assets and zero debt. SIS has built a $66M revenue business with $83.7M in assets and $20.9M in debt.

Maurten generates approximately $2 of revenue for every $1 of assets. SIS generates approximately $0.79 of revenue for every $1 of assets. That gap reflects the heavy acquisition spending and infrastructure investment SIS made during its growth phase, costs that are now weighing on the business without generating proportionate revenue returns.

Differing private equity philosophies

IRIS Ventures backing Maurten is a growth equity bet. They are investing in a business that has proven the model works, is growing fast, and needs capital to scale further. Can Maurten sustain growth and expand margins simultaneously? The last two years say yes but the story is still early.

BD Capital backing SIS is a turnaround and restructuring bet. They are investing in a business with historic brand equity, an established customer base, and workable gross margins, but one that has not managed its cost structure well enough to generate profit. The risk is transformation. Can BD Capital fix the cost structure, stabilize revenue, and create a path to genuine profitability that the public markets didn’t believe in? The normalized EBITDA improvement in FY2024 suggests the work has already begun.

What does the future hold?

Two companies with completely different backgrounds appear to be on a collision course. Maurten looks increasingly like the next market leader in premium endurance nutrition while SIS is relinquishing its throne after years of accumulated losses. Maurten is backed by venture capital looking to accelerate growth while SIS is undergoing what may be a significant restructuring under a private equity firm with a mandate to fix what the public markets could not.

If I had to place a bet on either company it would be Maurten, but SIS cannot be counted out entirely. A lot will have to go right for SIS to outmaneuver Maurten, and that tells us something important about what actually drives success in the broader performance-focused endurance market, whether it is nutrition brands, apparel companies, or bike manufacturers. Product education, athlete storytelling, and brand identity are what win in this space. Maurten has executed on all three with discipline. SIS needs to recenter on all three with urgency.

It may sound counterintuitive, but Maurten’s expanding commercial success is largely the result of dialing in those three areas within a very focused niche before expanding outward. SIS did the same thing, albeit much earlier, and is now struggling in the mass market it chased. Their most credible path forward may be narrowing their focus, rebuilding brand loyalty within a defined consumer base, and using that foundation to pursue more stabilized and sustainable growth.

Black and white: Maurten’s calculated ascent

Maurten’s entire brand identity is built around their black and white aesthetic. No thrills, nothing flashy, just high-carbohydrate, flavorless products engineered for peak human performance. When they entered the market they were not targeting the mass consumer. Anyone casually participating in endurance sports or new to performance nutrition is not going to gravitate toward a brand with flavorless products that might disturb an untrained gut. Those athletes will start with cheaper and more approachable brands with familiar flavor options like GU or SIS.

For performance-oriented athletes or those getting more serious about endurance, however, Maurten becomes genuinely compelling. Their distinctive branding, elite athlete partnerships, and clear product education make it easy for athletes to identify Maurten as best in class. Their packaging communicates exactly what you are getting, and their original product line is intentionally minimal, which makes the decision process simple. Gel or drink mix, with or without caffeine, and for their energy bar, plain or chocolate. That was essentially the entire decision tree.

As we are seeing today, that strategy has helped Maurten grow both their total addressable market and their product offering. Two recent releases paint a clear picture of where the brand has its sights set.

The first is Maurten’s education hub, which helps athletes determine fueling strategy across a variety of training and racing scenarios. Their product offering was already straightforward, but now they are closing the loop on any guesswork or research athletes would otherwise need to conduct to optimize their fueling with Maurten products.

The second is Maurten Additions. Maurten built its reputation on flavorless products, but they have now released four flavor options that athletes can add to their drink mix. The way they have rolled it out and marketed it is smart. By keeping the mix and the additions as separate purchases, Maurten has achieved two things simultaneously: streamlined production logistics and a dual marketing play that speaks to performance athletes while quietly opening the door to more mass market athletes getting into the performance side of endurance sports.

We have all read about brands dealing with inventory overhang since 2020, and for many the root cause is an expansive product offering that requires more raw materials and SKU management. If Maurten had chosen to pre-add flavors directly to their drink mixes, the number of SKUs, packaging variations, and distribution requirements would have multiplied significantly. Instead of going from three drink mix options to fifteen, they kept the core lineup at three and introduced four additions products. That is eight fewer new packaging designs and production methods to manage.

The marketing is also fully consistent with everything they have done before: performance forward. Additions are positioned as a tool for athletes to combat flavor fatigue rather than an alternative to the flavorless mix. The framing signals a continued focus on high-performance athletes, but it is subtly opening the door for more casual athletes who are accustomed to flavored products. Brand identity intact, market share gained.

Where SIS can learn and execute

If I were advising a private equity firm on SIS, there would be some immediate actions worth taking to help the brand regain its footing and more directly compete with Maurten. We just looked at Maurten’s strengths, and SIS has a real opportunity to put their own spin on each of them. There is risk involved, but in their current situation the clock is ticking. Risk is part of the equation now if SIS wants to reclaim ground from Maurten.

SIS is a legacy brand in endurance nutrition with a long-standing brand image. They were once the original science-first brand in the space, but that edge has clearly eroded. A rebrand could do the company significant good, and that rebrand can come from operational decisions rather than narrative alone.

Maurten has demonstrated that a focused product line goes a long way. SIS’s lineup of gels and drink mixes looks sprawling by comparison, and the root cause is that SIS essentially has two brands competing within the same portfolio. The first is their original line of isotonic gels and mixes that represent the brand’s heritage. Those gels fall behind modern performance standards at just 22 grams of carbohydrates per serving, and their original drink mix offers electrolytes without carbohydrates, which makes it a difficult sell in a market where athletes expect both in one product.

The second brand within their lineup is one I actually use regularly: Beta Fuel. Beta Fuel gels deliver 40 grams of carbohydrates and Beta Fuel mix delivers 80 grams per serving, putting them directly in line with Maurten’s product standards. The Beta Fuel branding is sleeker and more in step with modern performance positioning.

If SIS gutted their lineup and rebuilt around Beta Fuel exclusively, they would reduce their production footprint, free up capital, and achieve a meaningful rebrand that repositions them squarely against Maurten. The obvious risk is losing consumers who still rely on lower carbohydrate options. Maurten does offer lower carbohydrate versions of their products without separating them into distinct sub-brands. A simple solution for SIS would be introducing a lower carbohydrate Beta Fuel gel, preserving the unified brand identity without cutting off a meaningful segment of their existing customer base.

Remember how we discussed Maurten’s Additions line being a smart move? This is where SIS’s size could actually work in their favor. SIS already offers a wide range of flavors for Beta Fuel alongside their unflavored versions, and they do not require consumers to buy and mix two separate products. SIS already has the production infrastructure to support this volume of pre-flavored products, whereas Maurten would be burning significant brand and financial capital to expand their lineup in the same direction.

If SIS can amplify a rebrand and convincingly position Beta Fuel as a direct competitor to Maurten while being more approachable, they could flip the narrative and get back to revenue growth before their current collision course with Maurten becomes irreversible.

On the storytelling front, SIS needs to reinvest in meaningful partnerships and compelling narratives. SIS is a British brand that lost Britain’s most iconic cycling team, Ineos Grenadiers, to Maurten. That is a significant blow to brand identity, and it feels like little has been done to confront that reality head on. With capital freed up from cutting underperforming product lines, SIS should reinvest in storytelling that resonates with younger audiences the way Maurten’s does. As we have seen time and time again in endurance sports, story is the most powerful marketing tool in the game.

Two paths to victory

I always enjoy doing these financial deep dives, and I want to be clear that this is all my outside perspective. I could absolutely be missing context, but I do think these comparisons reveal the different financial levers being pulled across endurance sport right now. We are at a cultural inflection point where endurance sports are growing in popularity every day, and certain brands will capitalize on that while others will not. Both Maurten and SIS have meaningful capital behind them, but the investment philosophies could not be more different.

Through Built on Bikes we have explored how newer brands like Pas Normal Studios and Ventum are finding success, and how established brands like ENVE and Rapha can build on their strengths and right a struggling ship. Both possibilities are very much on the table for Maurten and SIS. My advice is simple: keep an eye on both. Maurten will continue to grow in ways that are hard to ignore, but do not sleep on a quiet comeback from SIS.

In other news…

Veronica Ewers gives inside perspective on pro friendships

Check out Veronica’s latest Substack post where she illustrates the often black and white relationships that professional cyclists have. One moment you could be on a team and everyone feels like family and the next you are off the team having no communication with people that played a massive role in your life.

Andrew Vontz is kicking cancer’s ass

Andrew Vontz, author of the Choose the Hard Way newsletter, has become a great friend since I started Built on Bikes. We were deep into scheming networking ideas for Unbound when he was diagnosed with cancer. Since then he has been riding the waves with incredible resilience, putting out content that offers genuine perspective and inspires you to reframe your own challenges. He also still manages to crack great jokes from the chemo ward. My personal favorite: “I’m the Strava local legend of the chemo ward.” Check out his Substack and podcast.

I might go dark next week

Fresh off my article on AI training solutions, I was approached by a company that claims to do everything I described in that piece. Over the last month I have had the opportunity to speak with their executive leadership team multiple times, and I will be writing a comprehensive article on the company. It will not be possible to do the story justice in a single week, so I may need to take a week off from the usual publishing schedule to bring it to you in its fullest form. If I do not post next week, that is why. And if I do post, expect something shorter than usual.

I’ll be at UNBOUND!

That is right, I will be at the biggest gravel race in the world at the end of May. I will be there supporting the Mach1 Devo Team but will also be hopping around to network. If you will be there, let’s connect: [email protected]

Ride and rip,

Kyle Dawes

Nice article thanks. Surely Precision needs to be spoke about in this company or their market cap not there yet?

Is it just me or is Maurten, SIS, and Never Second's branding and marketing nearly identical? Especially with the black packaging. On the other hand I love Carbs Fuel's white packaging, though I am biased because I am friends with the Carbs founders.